Towards new data driven methods for financial audits

The application of network theory in financial audits

15 December 2020

New financial audit methods

Despite the growing interest in applying data driven methods in audit and the availability of large volumes of digitally recorded data, audit methods are mostly manual in nature, and developing an algorithmic equivalent proves challenging. Data used in these algorithms are recorded at the most detailed level, individual transactions that pertain to the company. But auditors provide trust about financial statements (the summed totals of individual transactions), not individual data points. To develop data driven methods, understanding the link between the low-level recorded data and its aggregate representation is therefore essential.

Marcel Boersma (PhD candidate from KPMG and Computational Science Lab University of Amsterdam), Dr. Sumit Sourabh and Prof. Dr. Drona Kandhai of the Computational Science Lab, together with Aleksei Maliutin and Lucas Hoogduin from KPMG as industry partner, developed a data driven technique that makes it possible to consistently and objectively analyze vast amounts of data and thereby potentially improve the audit quality. Other potential applications include fraud analytics.

Network theory

Boersma i.a. developed a method that turns low-level financial transaction data – for example data that records that the entity sold an item and earned revenue – into a bipartite network representation (Boersma et al. 2018, Boersma et al. 2020). The network shows an overview of all the monetary flows within the financial system, moreover it also shows which process – e.g., the sales process, the salary payments process – drives the monetary flow. This network enables the researchers to capture the interconnectedness of the company’s financial system from individual data points and link this to the high-level aggregates presented in the annual reports in a data driven way.

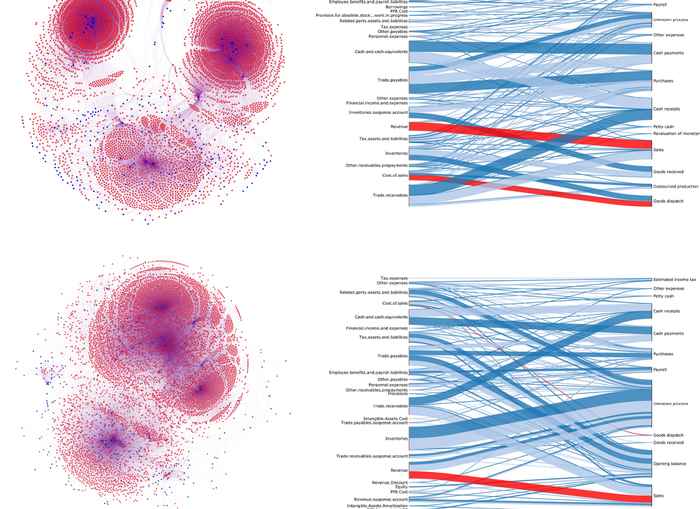

Figure 1

In Figure 1 left, is the network extracted from one year of transaction data. This representation is simplified by grouping similar nodes, Figure 1 right shows the simplified monetary flows within the financial system. This enables the auditor to have an overview of the monetary flows and detect unexpected monetary flows from data. The auditor can adjust its audit approach accordingly. Moreover, they look for the dynamics on the process level that result in relationships between monetary flows (edges). These relationships can be used to monitor whether monetary flows are consistent with their expectations, significant deviations from the expectations are a reason to investigate further.

Boersma i.a. believe that methods, as presented by them, can pave the way towards a more data driven audit.

Boersma, M., Sourabh, S., Hoogduin, L., & Kandhai, D. (2018). Financial statement networks: an application of network theory in audit. The Journal of Network Theory in Finance, 4.

Boersma, M., et al. "Reducing the complexity of financial networks using network embeddings." Scientific Reports 10.1 (2020): 1-15.